How to pick an informed separation and divorce mortgage strategy for your

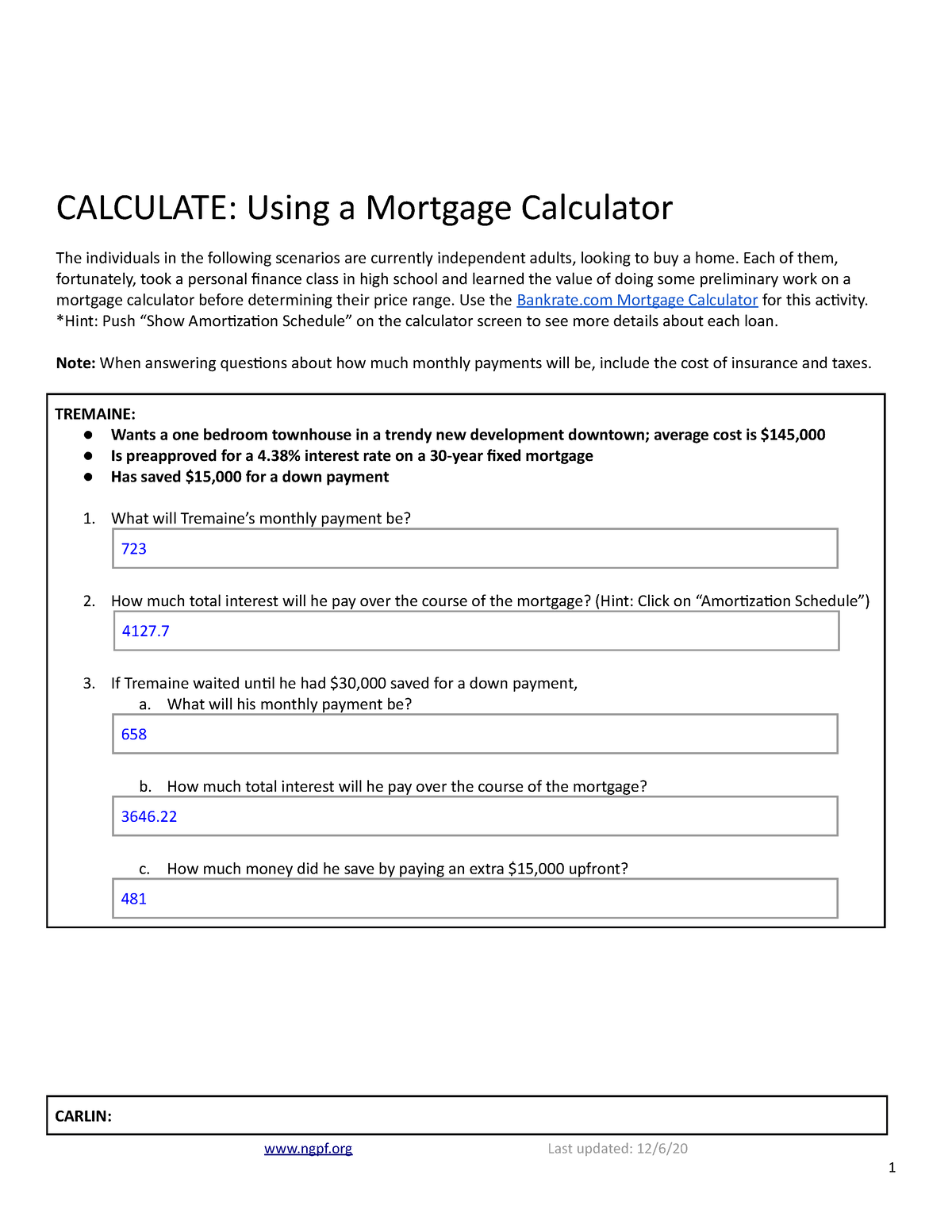

Divorce proceedings and you will mortgage factors will put complexity so you’re able to a currently problematic procedure. With a joint home loan regarding combine, navigating a separation and divorce need careful believed.

But really, demonstrated breakup home loan methods will assist each party. Such measures are different, with regards to the house’s security, the acquisition and you may identity information, assuming one to lover intentions to preserve control.

Exactly what are your own divorce financial alternatives?

When you look at the a separation, exactly who gets the home is a primary choice that often is based into divorce and financial information. If your label actually towards the mortgage, information their liberties is important. It’s also important to know how split up impacts your home financing and mortgage responsibilities.

step 1. Refinancing mortgage after divorce

During the a splitting up and you will home loan, refinancing current financial having only 1 partner’s name’s often the cleanest provider when you look at the a split up.

Adopting the home loan re-finance shuts, precisely the people entitled to your mortgage might be accountable for putting some monthly payments. The person not any longer called with the home loan you may after that become taken out of the latest house’s term.

- Example: what if John and you will Jennifer together individual a property valued within $three hundred,000 with a remaining home loan balance off $2 hundred,000. It pick Jennifer helps to keep the house. Jennifer you can expect to re-finance the mortgage into the their own title alone to have $250,000. She’d have fun with $2 hundred,000 to settle the original mutual mortgage, following spend John the rest $50,000 for his display of equity.

If required, a money-aside refinance you will definitely pay the portion of guarantee that is due brand new departing lover. Refinancing into the a special financial may be the greatest provider, nonetheless it functions only if that lover can be eligible for the fresh new loan by themselves. Home loan qualification is determined by this type of situations.

Borrower’s income

Just one borrower will produces lower than a couple, so it is more difficult so you can qualify for home financing individually. From inside the underwriting processes, the lender often be certain that new single borrower’s earnings and you may examine it on their month-to-month costs, together with bank card minimum payments and you will car money. Should your solitary borrower’s income can secure the the fresh new loan’s home loan fee, up coming refinancing is a money loans in Cheraw possible choice.

Borrower’s credit score

The person refinancing the borrowed funds loan need to have a top sufficient credit score in order to qualify. Should your credit scores has actually fallen since you grabbed from most recent real estate loan, you can also no further be eligible for a good refinance. Specific financing programs such as for example FHA, Virtual assistant, and you may USDA fund have more lenient credit score requirements, normally making it possible for scores as low as 580 oftentimes.

You’re in a position to improve your borrowing that have a-sudden rescore, however, reconstructing borrowing from the bank is often the only solution for the lowest credit rating, that take weeks or ages.

Borrower’s home equity

Restricted equity out of a recent pick, short deposit, or next mortgage is hinder refinancing. Conventional financing usually wanted no less than step 3% home guarantee, if you’re FHA and you may Va fund succeed refinancing with little to no collateral sometimes. Loan providers get telephone call so it your loan-to-value ratio, otherwise LTV. A home having 3% collateral could have an LTV out-of 97%.

2. Refinancing with reasonable house collateral

Particular refinance solutions will let you eliminate a wife or husband’s title out-of the original financial, despite an excellent residence’s reasonable security status.

FHA Streamline Re-finance

For those who currently have an enthusiastic FHA financing towards the house, you should use the newest FHA Streamline Refinance to remove a borrower versus examining domestic collateral. not, the remaining partner need certainly to reveal that these are generally making the whole mortgage repayment for the past half a year.